Economic Snapshot – The Architecture Industry – Special Analysis

The Architecture Industry serves an integral role in the operations of Israel’s Real Estate Industry. Accordingly, the dynamic activity in the real estate industry over the past few years should have led also to a prospering architecture industry. In actuality, despite the work loads in the market, the architecture industry is facing several material challenges, including a shortage of high-quality human resources and the difficulty to retain existing human resources, the lack of competitiveness of small and medium firms compared with the larger firms which receive most of the larger projects, the low payment ethics of the customers which disrupts the cash flows of architecture firms and more.

As a profession, architecture requires a long period of training, that includes 5 years of studying for a degree in one of five academic institutes that have such programs in Israel (Tel Aviv University, Technion, Vizo Haifa, Bezalel and Ariel University). After graduation, one may receive the title of a Registered Architect, who has limited planning authorities, for buildings with a height of up to 12 meters, such as private houses. Most graduates continue with a 3.5 years long internship, after which they are required to pass two exams, theoretical and practical, in order to receive their Licensed Architect from the Ministry of Labor and Welfare; this provides them with unlimited planning authorities. Over the past few years, 300-400 architects have been licensed by the Ministry of Labor and Welfare annually, after completing all of their license stages, with the expectation of being hired in the market.

As of 2019, there are about 11,000 registered and licensed architects in Israel, of which only about 6,000 are active in the market. This results from the relatively low pay levels in the industry, particularly for young architects, and the filling of architect jobs by architecture practical engineers, who receive authorities that are identical to those of registered architects, through a fast certification proceeding.

About 3,000 architecture firms operate in Israel, a large part of which are small firms with 2-3 employees or independent architects.

The industry is affected by the uncertainty in the real estate industry following the elections, a lack of certain outlook for the continuing implementation of the “Mehir LaMishtaken” (government price-capped) program, policy changes in the local authorities on urban renewal and more. It should be interesting to follow the developments in the real estate industry over the next year, particularly in the urban renewal field, and their consequent effects on the architecture industry. An extension of the Tama 38 program, if it would be renewed, is expected to release delayed permits to the market and benefit the industry.

In light of the industry trends, D&B estimates that more than half of new architecture firms don’t survive their fourth year.

The Effects of the Real Estate Industry

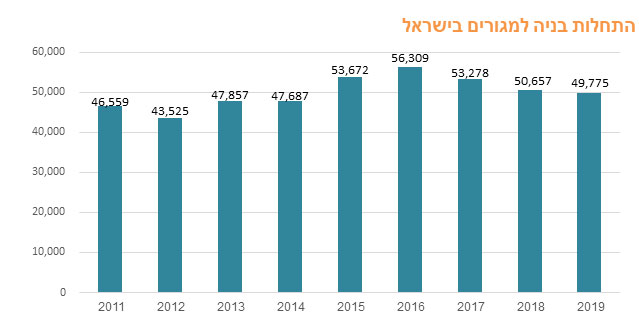

The residential real estate industry experienced a slowdown in 2017-2018, compared with its activity levels in previous years, while shifting the focus to Mehir LaMishtaken projects and in the free market – to focusing on urban renewal projects.

The slowdown halted in the first half of 2019, as expressed both in the number of new apartments sold and in the number of construction starts, while stabilizing at lower levels than those of previous years.

Residential Construction Starts in Israel

Source: The Central Bureau of Statistics, Processed by D&B.

* 2019 data is estimated

The government has been focusing, over the past few years, in the Mehir LaMishtaken program, and this led to lower construction starts in non-Mehir-LaMishtaken projects – less projects for the contractors to compete on. Starting from the second half of 2018, a decline was recorded also in the construction starts of Mehir LaMishtaken program, a trend which continued into 2019.

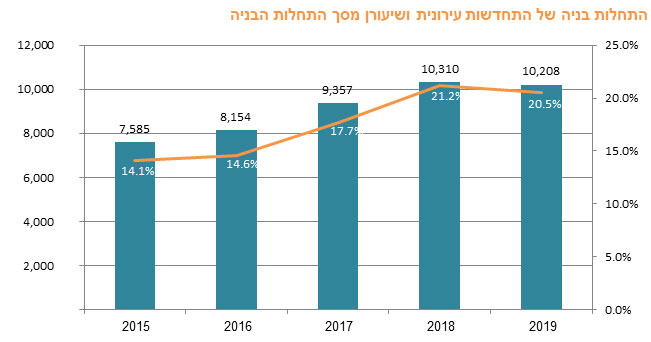

In contrast with the decline of the total number of construction starts, the share of urban renewal construction starts of total construction starts has been increasing in recent years, and in 2018 was more than 20% of total construction starts, a trend which continued also into the first half of 2019.

Urban Renewal Construction Starts and their Share of Total Construction Starts

Source: The Central Bureau of Statistics, Processed by D&B.

* 2019 data is estimated

2019 has been characterized by uncertainty in the urban renewal field – in this framework, several local authorities changed their policies in this area. In addition, the industry focus might shift in 2020 – to the execution of large complexes (Pinui-Binui), without additional small-scale Tama 38/1 projects – thus, in July 2019, the Planning Administration has announced its intention not to extend the validity of the Tama 38 program in its current format (the current plan will expire in May 2020), while shifting the focus of operations to the planning of large-scale neighborhoods (in large Pinui-Binui complexes). This announcement generated turmoil among various players in the industry and gave rise to public interest in this matter. Despite the uncertainty in the industry, this field maintained relative stability in its operations in the first half of 2019 YoY.

The Architecture Industry – Main Challenges

- Low payment ethics of the customers: Most of the industry’s customers are government entities, municipalities and real estate developers. These customer typically present long collection periods (“credit days”). Architecture firms face collection difficulties, which threaten the firm’s cash flows, and are passed on to the employees and create unattractive salary level for architects.

- High uncertainty in light of the exposure to real estate: While discussion are held on the future implementation of urban renewal, the future of the Mehir LaMishtaken program is even less certain, in light of the uncertainties of an election year and the future policy of the new government. We note that after several months during which no Mehir LaMishtaken draws were carried out, in late September 2019 the ninth draw (“The Big Draw”) was opened, and it will include more than 3,000 apartments in 13 towns across Israel. A slowdown in the real estate sector is expected to lead to a slowdown in the architecture industry as a supplementary industry.

- A difficulty in retaining high-quality human resources: the industry’s low pay levels lead to a rush of employees to the large firms, which can pay more, on the expense of small and medium firms, or to retiring in order to open independent firms (with a survivability chance that isn’t very high). In addition, in a considerable number of cases, the low salary levels lead architects to leave the industry (to higher-pay fields such as construction inspection etc.). In addition, while architects are required to undergo a long period of training, in recent years more and more architecture practical engineers (who undergo a shorter training program) take the place of architects in various architecture firms.

- A Concentrated Industry: A high barrier of entry for new firms – the architecture industry is considered to have high industry-concentration, where the bigger customers work with the same firms (the larger firms) while small and medium firm can’t compete on such projects. this serves as a high barrier of entry for new firms, which are unable to receive works from large customers from the start. This trend supports to low survivability of new firms – as mentioned above, more than 50% of the new firms will not survive their fourth year.

- Bureaucracy and Red Tape – long processes: as a supplementary industry of the real estate industry, the architecture industry is also affected by the bureaucracy and the long processes that characterize the real estate industry, in particular in all aspects of receiving project permits.

Complete the following details and our Dun & Bradstreet

experts will guide you in finding your optimal solutions:

the form was submitted

Thank you for registering to dunsguide.

We will come back shortly

Dun & Bradstreet

Global Solutions

Business Promotion

Business Protection

Personally Tailored Solutions

Articles

All Rights Reserved 2023 © Dun & Bradstreet Israel Ltd.